Table of Content

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next. Victoria Araj is a Section Editor for Rocket Mortgage and held roles in mortgage banking, public relations and more in her 15+ years with the company. Based on the information you have provided, you are eligible to continue your home loan process online with Rocket Mortgage. Approval online today and see the difference a co-signer can make. If you’re struggling financially and you can’t find someone willing to co-sign on your loan, there are still a few ways you can buy a home.

The potential downside of getting a personal loan with a co-signer is that you can damage their credit if you miss a payment or default. Before you ask someone to cosign, inform them of the risks and make sure they understand their rights as a co-signer. Our advertisers do not compensate us for favorable reviews or recommendations. Our site has comprehensive free listings and information for a variety of financial services from mortgages to banking to insurance, but we don’t include every product in the marketplace.

Check Rates

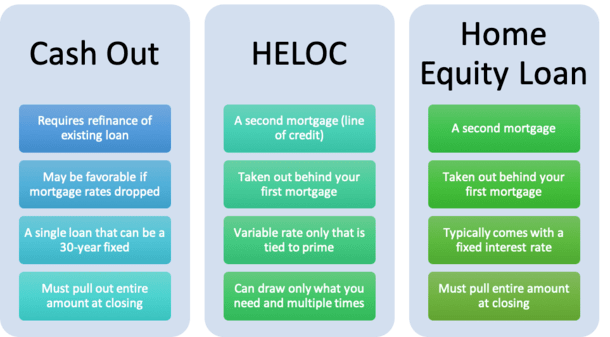

Get documentation in writing that the lender should contact you if the primary borrower defaults. By getting immediate notification, you may make the payment on the primary borrower's behalf and save your credit standing. You need more than property equity to qualify for a home equity line of credit. Like all credit, home equity loans are based on your income level and past credit history.

Home equity loans can be a convenient source of funding when you need cash for different financial goals. If you co-own a home with someone to whom you’re not married, it’s important to discuss whether it makes sense to apply for a home equity loan together. Talking to a mortgage expert can help you understand which rights and responsibilities apply when taking out a home equity loan with or without the property’s co-owner.

Co-Signers and Home Equity Loans

The operator of this website is not a lender, does not broker loans to lenders and does not make personal loans or credit decisions. This website does not constitute an offer or solicitation to lend. This website will submit the information you provide to a lender.

Foreclosures can cause you to lose points from your credit scores. They can also remain on your credit reports for up to seven years. Eligibility for a home equity loan or HELOC up to $500,000 depends on the information provided in the home equity application. Loans above $250,000 require an in-home appraisal and title insurance. For HELOCs borrowers must take an initial draw of $50,000 at closing.

Editorial integrity

Subsequent HELOC draws are prohibited during the first 90 days following closing. After the first 90 days following closing, subsequent HELOC draws must be $1,000 or more . A co-applicant with good credit could improve approval chances for a primary borrower with shakier. Not only that, you might be able to access more equity in your home by applying for a HELOC with a co-applicant. The loan-to-value ratio is a lending risk assessment ratio that financial institutions and other lenders examine before approving a mortgage. This doesn’t mean, however, that one co-owner can take out a home equity loan without the consent of the other co-owner.

This means that when you’re a co-signer, the lender can come after you for payments if the primary signer defaults on the mortgage. The lender has the right to hold you responsible for the missed loan payment even if you don’t live in the home. Today, we’re looking at what it means to be a nonoccupant co-client – or co-signer – on a mortgage loan. In this article, we’ll show you what co-signing means and when it’s beneficial. We’ll also introduce you to the drawbacks of being a nonoccupant co-client and some of your other options as a borrower.

Banks and lenders approve loans based on the applicant's credit history, credit rating and income, among a few other factors. If the applicant is denied credit approval by the bank, he can re-apply with a more qualified cosigner to obtain the loan. When applying for a home equity loan with a cosigner, the cosigner does not need to be on the deed to the property. Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions.

This law changed some of the rules for deducting home equity loan interest and caused some confusion. As of 2018, taxpayers can deduct the interest paid on a home equity loan amount up to $750,000. The law only allows this deduction if you used the loan money to make improvements or repairs to the home.

The lender will calculate the debt-to-income ratio using both credit reports and both sets of financial documents. If you qualify with the co-signer, the process will move forward. The co-signer uses his good credit history or higher income to secure the loan for the primary applicant.

Getting a home equity loan with bad credit isn’t impossible, though. Once the loan is closed, both you and the co-signer are on the hook for the payments. It doesn't matter to the lender whether one or both of you make the payments as long as they're paid. If you fail to make the payments, however, it can take legal action against both of you. If, eventually, you wish to remove the co-signer, you will have to prove that you can afford the payments on your own. If the lender determines the co-signer is no longer needed, you'll have to sign a modification or an entirely new set of documents depending on the lender's policy and procedure.

Community banks and credit unions might have more flexibility when it comes to their underwriting standards than big banks do especially if you are already a customer there. They also have to compete harder for business, and may be willing to take on riskier loans. Once you are ready to close, the co-signer attends settlement with you. You both sign the promissory note, which is the contract between you and the lender. With both of you signing the note, you are both obligated for the repayment of the loan. The mortgage document, which serves to pledge the collateral, will be signed solely by you, since you are the owner of record.

If you're interested in a credit-builder loan, check your local banks and credit unions. You could get around that issue if you had a cosigner, as the lender would use that person's credit in the decision instead of yours. But without a cosigner, you have to rely on what you do have – income and collateral. Opinions expressed here are the author’s alone, not those of an issuer, and have not been reviewed, approved or otherwise endorsed by an issuer. Please keep in mind that while some offers may come from WalletHub advertising partners, sponsorship status played no role in loan selection. WalletHub makes it easy to find the best personal loan with a cosigner.

How We Make Money

From here, your mortgage generally functions the same way it would if you were the only person on the loan. You make a premium payment every month to cover your principal, interest, taxes and insurance , and you enjoy your home. However, the lender may hold the nonoccupant co-client responsible if you miss a payment. This means your lender has the right to take your mother to court and force her to repay the loan. Another important ratio is your combined loan-to-value, or CLTV, ratio, which is the ratio of all outstanding loans secured against your property divided by your home's current value.

Two people who own a home together but are not married can take out a home equity loan jointly, assuming that they’re each able to get approved by the lender. If a co-owner would prefer not to be added to the loan, the other homeowner can still apply with some stipulations. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy. If the primary occupant misses a payment, your credit will suffer as well. If you’re being asked to co-sign a mortgage, it’s important that you’re aware of all the long-term negative consequences that could result from the occupying borrower’s default. Becoming a nonoccupant co-client means you’re just as legally responsible for the loan as the person living in the house.

No comments:

Post a Comment